Article by Violeta Todorova

UnitedHealth Surges After Strong Q1 and Raised Guidance

April 23, 2026 | Research Insights

UnitedHealth Q1 Earnings Top Estimates and Boosts 2026 Guidance

UnitedHealth delivered a solid top- and bottom-line performance in Q1 2026. Revenue rose 2% year-on-year to $111.7 billion, while adjusted earnings per share came in at $7.23, comfortably ahead of consensus estimates1.

Management raised its full-year 2026 outlook, now expecting adjusted EPS of more than $18.25, up from prior guidance of $17.751. This upgrade played an important role in changing market sentiment, reinforcing the view that the company’s operational reset is beginning to translate into measurable financial performance.

Shares of UnitedHealth Group surged following its first-quarter 2026 earnings release, with the stock rising around 7%. The rally was driven by renewed investor confidence after one of the company’s strongest quarters in recent years.

The strong reaction in the share price suggests investors are willing to reprice the stock based on improved execution rather than past concerns. Yet, despite the headline beat, the improvement in fundamentals faces lingering structural and macro risks.

Medical Cost Improvements Provide a Key Catalyst

A major driver of the earnings upside was better-than-expected cost control. The medical cost ratio, which is a key profitability metric declined to 83.9% from 84.8% a year earlier, coming in below analyst expectations1.

This improvement reflects stronger cost discipline, favourable reserve development, and early benefits from operational restructuring. This was one of the most important factors supporting the post-earnings rally, as elevated medical costs have been a persistent overhang on the stock in recent quarters.

However, management cautioned that underlying cost pressures remain “consistently elevated,” suggesting that while the worst may be behind, the margin recovery is still in progress.

Mixed Results Across UnitedHealth Segments

Despite the strong headline results, performance across business segments was uneven. The core insurance division, UnitedHealthcare, delivered steady growth, with revenue rising to $86.3 billion, supported by premium increases and resilient demand1.

Meanwhile, Optum which is the company’s healthcare services arm presented a more mixed picture. Optum Rx showed continued strength, but Optum Health experienced a decline in revenue and operating income, reflecting fewer value-based care members1.

These divergences highlight that while the overall business is stabilising, certain segments are still in transition, which could limit the pace of earnings expansion in the near term.

AI and Operational Transformation Support Long-Term Growth

A key pillar of UnitedHealth’s improving outlook is its continued investment in digital transformation and artificial intelligence. Management highlighted that AI-driven efficiencies, pricing discipline, and expanded value-based care models are already contributing to better operational outcomes2.

With approximately $1.5 billion allocated to AI initiatives, the company is targeting improvements in administrative efficiency, care delivery, and cost predictability. Early indicators, including increased digital engagement and faster processing times suggest these investments could support both margin expansion and revenue growth over time2.

This strategic move positions UnitedHealth to enhance scalability and potentially unlock new revenue streams, particularly through its Optum platform.

Balance Sheet Strength and Cash Flow Provide Stability

From a financial standpoint, UnitedHealth remains well-capitalised. The company generated $8.9 billion in operating cash flow during the quarter and increased its cash position to over $31 billion1.

At the same time, leverage remains manageable, with a debt-to-capital ratio of 42.9%. This financial flexibility allows the company to continue investing in growth initiatives while returning capital to shareholders through dividends and buybacks.

Such balance sheet strength is a key factor supporting the stock, particularly in the current macro environment.

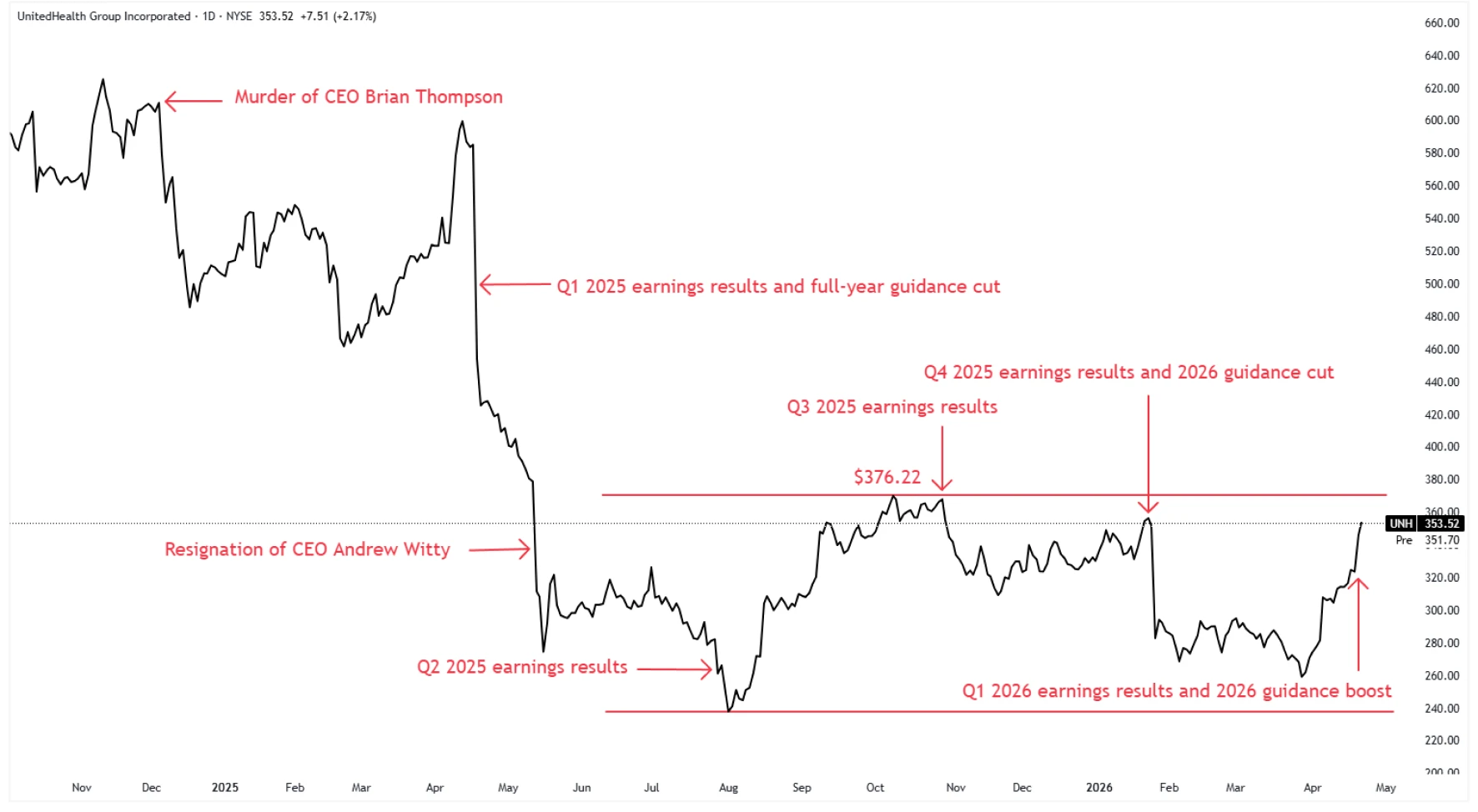

Source: TradingView. UNH daily price chart, as of April 22, 2026

UnitedHealth Rally Signals Turnaround, But Risks Remain

The post-earnings rally signals a potential inflection point for UnitedHealth’s share price, given that the stock remains significantly below its previous highs.

In the near term, momentum could be supported by improving margins, raised guidance, and growing confidence in management’s turnaround strategy. The results are evidence that the company may be returning to its historical “beat-and-raise” pattern from the past1.

However, risks remain. Elevated medical costs, regulatory uncertainty, and continued weakness in parts of the Optum business could create volatility. Additionally, broader healthcare policy changes, particularly around Medicare and Medicaid represent an ongoing overhang.

As a result, the stock’s trajectory is likely to remain closely tied to execution. Sustained margin improvement and consistent delivery on guidance will be critical for further upside.

From a technical analysis perspective, the stock has been in the process of building a large base since August 2025. Strong signs are emerging that the price has bottomed at $234.60, and we see good probability of a reversal of the prior down trend this year. A break above key resistance of $376.22 appears increasingly likely and would act as a confirmation that a new primary up trend is starting. Upon confirmation, the stock could easily rally to $460 over the long-term.

Conclusion:

UnitedHealth’s Q1 2026 earnings mark a clear step forward, combining solid financial performance with improving operational metrics. The results have helped restore investor confidence and reposition the stock as a potential recovery play within the healthcare sector.

However, the path ahead is not without challenges. While the foundation for growth appears stronger, the sustainability of this momentum will depend on continued cost discipline, successful execution of strategic initiatives, and a stable regulatory environment.

In this context, UnitedHealth is transitioning from a period of uncertainty toward one of cautious optimism, where performance will drive the next phase of the stock’s re-rating.

Key Takeaways

Strong Q1 earnings and raised guidance boosted investor confidence and share price

Medical cost improvements supported margins, but pressures remain elevated

Mixed segment performance and regulatory risks could impact near-term momentum

Footnotes:

1UnitedHealth Group Reports First Quarter 2026 Results, as of April 21, 2026

2The Globe and Mail, UNH Q1 Deep Dive: AI Investment and Value-Based Care Drive UnitedHealth’s Strong Start, as of April 22, 2026