Adobe stock has significantly underperformed its peers within the Technology sector recently. Currently, it’s trading near $350 - more than 40% below the level it was trading at early last year.

Is the software stock capable of staging a recovery? Let’s take a look at the setup.

Why Has Adobe Stock Dropped?

The main reason Adobe stock has underperformed since early last year is that investors are worried about the impact of artificial intelligence (AI) on the business. There are a couple of factors at play here.

First, investors are concerned about Adobe’s ability to monetize its flagship generative AI offering, Firefly. This is a powerful tool that enables users to create and edit images and videos for commercial purposes through basic text prompts without facing copyright challenges. However, the issue is that Adobe faces significant competition in this space from the likes of Sora, Runway, Stable Diffusion, and Midjourney and therefore monetization could prove to be challenging. "We see increasing concerns surrounding competitive pressures and a longer time horizon to reach notable AI monetization," wrote analysts at CFRA Research in July.

Second, there’s a narrative in the market - which originated from Melius Research - that AI is going to “eat” software. The logic here is that AI automation in the years ahead will reduce the number of licenses or “seats” that software firms like Adobe can charge businesses for, shrinking their addressable markets and profit margins. On Adobe specifically, Melius1 recently cut its estimates and is now forecasting 7% revenue growth in FY2026 and just 4% growth in FY2027. It expects to see downward earnings revisions over the next four to eight quarters and has set a price target of $310 for the stock.

Can the Stock Recover?

Given this backdrop, a few things would most likely need to happen for the stock to see a material rebound. For a start, Adobe would need to show that it is capable of monetizing its AI offerings.

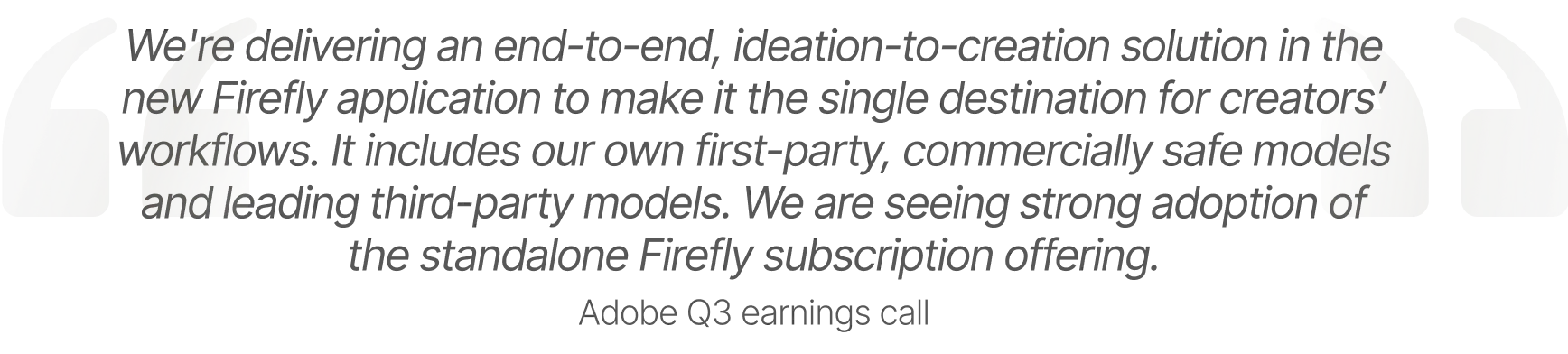

Now, there are some encouraging signs here. For example, on the company’s recent Q3 earnings call2, it said that Firefly is seeing strong adoption (Firefly app monthly active users grew 30 percent quarter over quarter), and that its AI-influenced annual recurring revenue (ARR) had topped $5 billion, up from $3.5 billion at the end of last fiscal year.

One factor that could potentially help Firefly gain traction is commercial safety. "We still have lots and lots of customers for whom taking stuff to production, they will only use Firefly because the commercial safety really matters to them," said Ely Greenfield, Adobe's Chief Technology Officer for Digital Media, in an interview with Reuters.

Another is integration of leading third-party models. Currently, Firefly supports Google’s Imagen, Veo, and Gemini Flash 2.5, OpenAI’s GPT-image, as well as, Flux, Runway, Ideogram, Pika, and Ray2.

Investors will also want to see that AI automation is not hurting Adobe’s subscription business model. It’s worth noting here that on the recent earnings call, management said that it is still seeing seat expansion in the enterprise, and that it can still win even if automation leads to less seats.

Finally, investors will want to see a pickup in top-line growth and consistent earnings beats and raises. The good news here is that in September, the company raised its guidance for the current quarter and said that it expects annualized revenue in its digital media business to increase 11.3% for the fiscal year, up from a prior forecast of 11% growth.

Trading At a Low Valuation

If the company can show traction in Firefly and an acceleration in growth, there is plenty of scope for an upward valuation re-rating. Currently, the stock is trading at just 17.0 times this fiscal year’s earnings forecast, a below market-average earnings multiple.

Using next fiscal year’s earnings forecast, the price-to-earnings (P/E) ratio falls to just 15.1 - an incredibly low valuation for a software company with a strong long-term track record and high profit margins. Note that with earnings per share growth of 12.3% projected next fiscal year, the price-to-earnings-to-growth (PEG) ratio is only 1.2.3

It’s worth pointing out that while Wall Street analysts have been lowering their EPS forecasts and share price targets for Adobe recently, the average price target is significantly above the current share price. Currently, it stands at $464, implying upside of around 30%.

Given the low valuation, and the average Wall Street price target, this could be a tech stock to keep an eye on. Especially around late October, when Adobe MAX takes place and the company shows off its latest generative AI technology.

Footnotes:

1Yahoo Finance, Melius Research warns that things ‘can get worse for SaaS players like Adobe’, as of August 11, 2025

2ADBE Q3FY25 Earnings Script and Slides, as of September 11, 2025

3LSEG, October 1, 2025