Earnings Beat, Outlook Miss

UnitedHealth Group’s latest earnings release delivered a mixed message to investors and the market’s verdict was swift.

On the surface, the quarter looked respectable. Adjusted earnings per share came in at $2.11, just ahead of consensus, while revenue climbed more than 12% year over year to $113.2 billion. Both UnitedHealthcare and Optum exceeded top-line expectations, highlighting the company’s scale and operational breadth1.

While the healthcare giant narrowly beat fourth-quarter earnings expectations and surprised positively on cost discipline, a rare revenue contraction outlook for 2026 overshadowed the results, sending the stock sharply lower and extending a bruising year for shareholders.

The reaction reflects more than just disappointment. It signals a broader reset in expectations for the managed care sector and a recognition that UnitedHealth’s turnaround will take time.

Revenue Warning and Medicare Pressure Rattle Investors

UnitedHealth Group shares fell sharply on Tuesday, after the healthcare giant warned that revenue is set to decline, unsettling investors already on edge about rising costs and regulatory pressure.

The company forecast a revenue contraction of at least 2% in 2026, guiding to more than $439 billion in sales, well below the $454.2 billion analysts had expected. UnitedHealth also projected adjusted earnings per share of at least $17.75 next year, alongside a medical care ratio of approximately 88.8%1.

The outlook caps a difficult period for the insurer. Medical spending has remained “historically high,” according to UnitedHealthcare CEO Tim Noel, while the company continues to face multiple civil and criminal investigations tied to its Medicare business. Leadership turnover has added to the uncertainty, with former CEO Andrew Witty stepping down in May and several senior executives exiting over the past year.

Adding to the pressure, the Trump administration announced that Medicare Advantage reimbursement rates will rise by just 0.09% in 2027, a sharp slowdown from last year’s 5.06% increase. The near-flat rate hike triggered a broader sell-off across the managed care sector, with UnitedHealth among the hardest hit2.

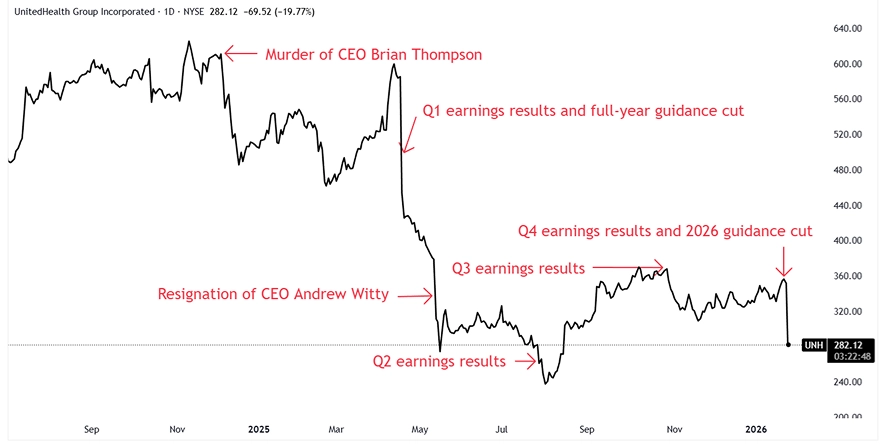

After the results, UnitedHealth fell sharply, pushing the stock to a near five-month low and extending its underperformance relative to the broader market. Over the past year, the shares lost more than 47% of its value and appear headed for further declines towards its key support of $235, before a recovery could be expected.

Source: TradingView, UNH daily price chart, as of January 27, 2026

Costs Are Stabilising but Still Elevated

One bright spot in the report was cost control. The company’s medical care ratio, which is the share of premiums spent on medical claims, came in at 88.9% for 2025, beating expectations and improving from earlier projections. Management guided to a slightly better ratio of around 88.8% in 2026, suggesting that pricing actions and benefit adjustments are beginning to gain traction1.

Medical cost inflation has been the industry’s biggest headwind, driven by higher Medicare Advantage utilisation, rising drug costs, and a post-pandemic return to deferred procedures. While costs remain historically high, executives emphasised that utilisation trends are no longer worsening, a subtle but important signal for margin stability.

Still, stabilisation is not the same as relief. Cost trends remain well above long-term averages, and government reimbursement is becoming less supportive.

A Company in Transition

UnitedHealth is going through a deep transition. Leadership changes, regulatory scrutiny, cyberattack fallout, and restructuring charges have all weighed on sentiment. The $1.6 billion charge tied largely to the Change Healthcare breach served as a reminder that operational risks can be just as damaging as medical costs1.

CEO Steve Hemsley’s return signals a renewed focus on execution, balance-sheet strength, and credibility. Management insists the company exited 2025 on firmer footing, but investors are clearly demanding proof.

Outlook for the Share Price: Stabilisation Before Recovery

From here, the path for UnitedHealth’s stock is unlikely to be smooth. Near-term momentum remains weak, and valuation alone may not be enough to attract buyers until revenue visibility improves. The market is no longer willing to price UnitedHealth as a low-risk compounder; it wants evidence that margins can expand even in a tougher reimbursement environment.

That said, expectations have been meaningfully reset. With earnings still projected to rise modestly in 2026 and cost ratios stabilising, downside risks may be narrowing. If pricing actions deliver as planned and Medicare utilisation continues to normalise, confidence could gradually return, but this looks more like a longer-term story.

Bottom Line

UnitedHealth’s earnings were not disastrous, but they were a reality check. The company is still highly profitable, operationally vast, and strategically important to the U.S. healthcare system. Yet growth is no longer guaranteed, and the margin for error has narrowed.

The message for investors is UnitedHealth is no longer a momentum stock. It is a turnaround in progress. The share price may stabilise around $235, but a sustained recovery will depend on execution, not assurances in an environment where costs, regulation, and scrutiny remain elevated.

Footnotes:

1UnitedHealth Group Reports 2025 Results and Issues 2026 Outlook, as of January 27, 2026

2CMS.gov, CMS Proposes 2027 Medicare Advantage and Part D Payment Policies to Improve Payment Accuracy and Sustainability, as of January 26, 2026