Salesforce stock has badly lagged the market in 2025. With AI promising radical transformation of business processes, investors have been concerned that the software company is vulnerable to disruption. Salesforce has been developing its own AI technology, however, to shift the narrative from AI disruption to AI dominance and protect its market share. And Q3 fiscal 2026 earnings1, posted on December 3, showed that the company is now starting to have significant success on this front.

Guidance Raised

For Q3, Salesforce posted revenue of $10.3 billion, up 9% year on year (8% at constant currency). Adjusted earnings per share came in at $3.25, up 35% year on year and well ahead of the consensus forecast of $2.862. Operating cash flow for the period was $2.3 billion, up 17% year on year, Meanwhile, free cash flow was $2.2 billion, up 22%.

Looking ahead, the company raised its guidance for fiscal 2026. It now expects revenue of $41.45 billion to $41.55 billion (from previous guidance of $41.1 billion to $41.3 billion), up 9% to 10% year on year. At the end of Q3, current remaining performance obligation (RPO) was $29.4 billion, 11% higher year over year. This signals a strong pipeline of future revenue.

Agentforce Momentum

Zooming in on the company’s AI platform, Agentforce, annualized recurring revenue (ARR) here jumped 330% year on year to $500 million in Q3. This growth was powered by a 58% quarter-on-quarter increase in customers paying for the technology, with 9,500 paying customers at the end of the period.

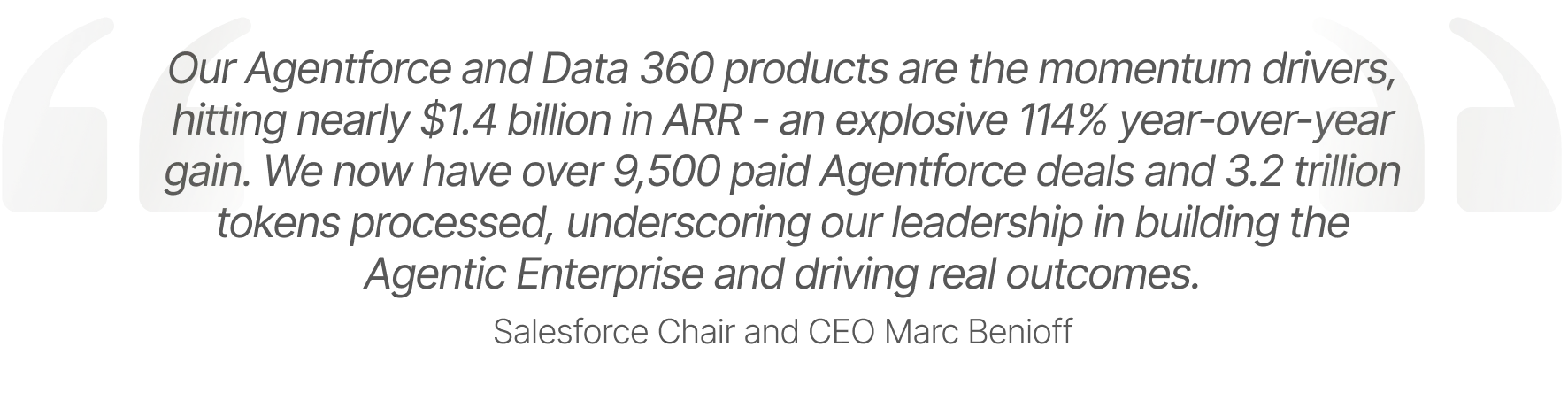

Agentforce and Data 360 ARR rose to around $1.4 billion, up 114% year on year. Note that 50% of Agentforce and Data 360 Q3 bookings came from existing customer expansion.

Given the Q3 momentum and continued Agentforce adoption, the company is targeting $60 billion plus in organic revenue by FY2030. It’s also targeting a profitable growth framework (the sum of its subscription and support constant currency growth rate and non-GAAP operating margin) of 50.

Earnings Call Insights

On the earnings call3, CEO Marc Benioff discussed investors' concerns in relation to AI disruption to its core business. His view is that it’s a “false narrative.” He went on to say that when building AI tools, the last mile is extremely hard because companies need data to provide the context. “For AI to be successful and accurate in the enterprise, you need the context. You need the data. You don’t want the agents to be essentially executing based on what they found in an LLM,” he said. Benioff stressed that Salesforce’s data infrastructure - which comprises Informatica, Data 360, and MuleSoft - is what makes the difference because this can provide the context for its AI tools. Next year, this area of the business is expected to generate around $10 billion in revenue.

Benioff also touched on the fact that existing customers are spending more on Agentforce. In Q3, 362 customers “refilled the tank,” according to the CEO. That compares to just three customers in Q1. “That’s an incredible testimony of the success that Agentforce is having in a very short time frame,” commented Benioff.

Analysts See Up to 70% Upside

Since Salesforce’s Q3 earnings, Wall Street firms have been adjusting their price targets4 for the software stock. Currently, many firms have price targets of $400, which implies share price upside of around 60%. Citizens currently has the highest price target on Wall Street at $430 - 70% higher than the current share price. The average price target is $328, implying upside of nearly 40%.

Footnotes:

1CRM Q3 FY26 Earnings Press Release, as of December 3, 2025

2CNBC, Salesforce beats on earnings, issues better-than-expected revenue forecast, as of December 3, 2025

3Investing.com, Earnings call transcript: Salesforce beats Q3 2026 forecasts, stock climbs, as of December 3, 2025

4Investing.com, Salesforce Inc (CRM), as of December 4, 2025