Article by Sandeep Rao

Why the ADR Listing Matters for SK Hynix Bull Investors

July 10, 2026 | Research Insights

SK Hynix – spun off from Hyundai in 2003 and acquired by SK in 2011 – has been a significant story in global semiconductors this year. With shares up roughly 280–300%1 in the year-to-date (YTD), the company briefly overtook Samsung Electronics to become South Korea's most valuable listed company with a market cap that touched approximately $1.2 trillion before a pullback that started in late June.

Presently, the bull case rests on two pillars: a dominant HBM market share amidst a memory supercycle that suppliers contend has years left to run, and a valuation that is sometimes argued as being cheap on forward earnings versus history and its U.S.-based peers with the potential for a structural re-rating made possible due to the listing of its American Depositary Receipt (ADR).

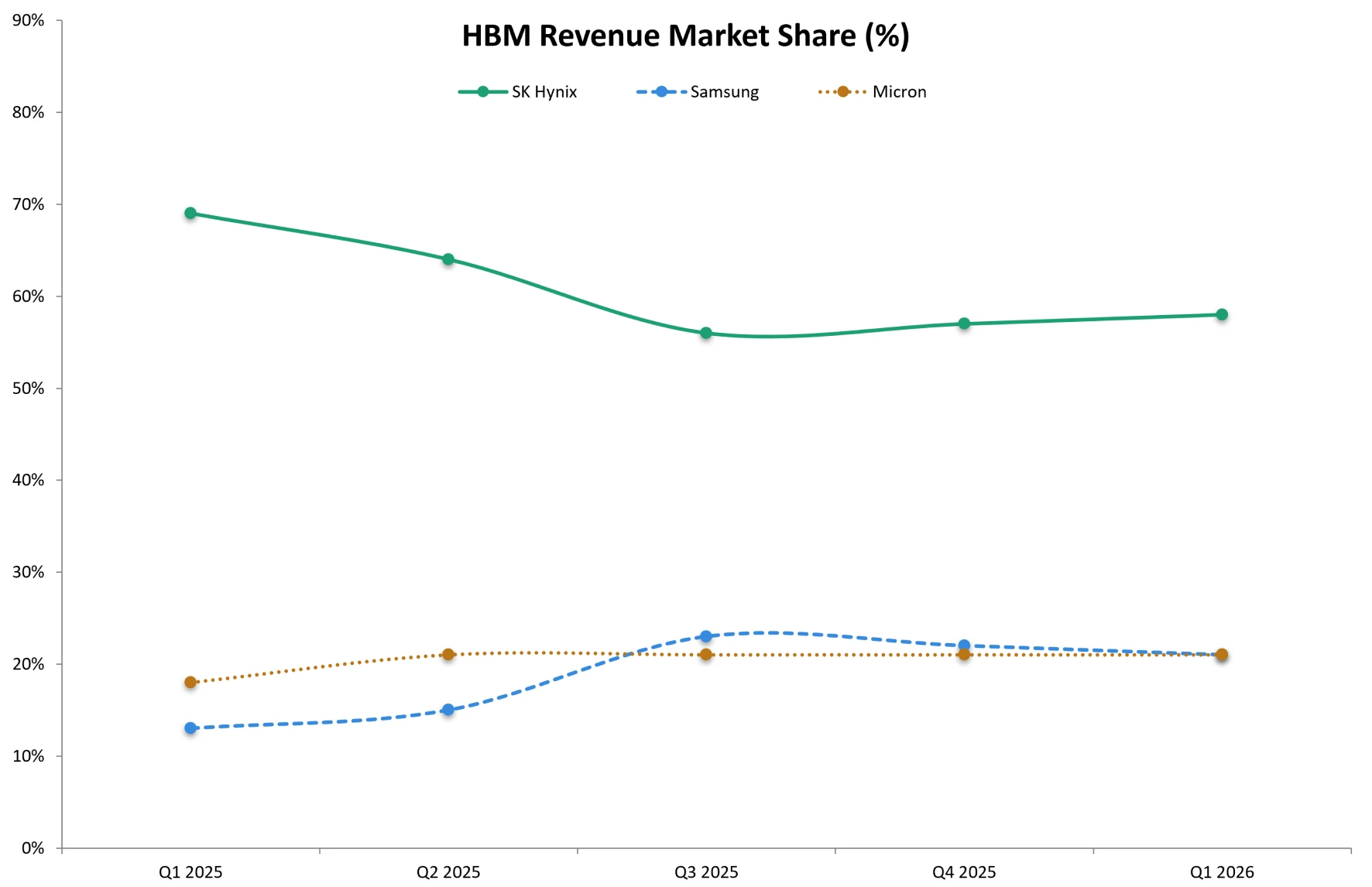

The HBM Dominance Thesis

SK Hynix controls an estimated2 58% of the market in High Bandwidth Memory (HBM) – a specialized, ultra-fast 3D RAM used in advanced GPUs and AI accelerators – where it competes mostly with Samsung and Micron.

Source: Counterpoint Research, Themes ETFs analysis, as of June 26, 2026

Earlier in June, the company recently showcased samples of 12-layer 48GB HBM4E – which can deliver per-stack bandwidths of up to and between 3.6 and 4.1 Terabytes per second (TB/s) needed for Generative AI and High-Performance Computing (HPC) – after developing an early lead by being integrated into Nvidia’s supply chain for HBM3E (which it delivers over 1.2 TB/s of bandwidth per stack).

This integration into Nvidia’s supply chain for premium-priced products had served it well: Q1 2026 revenue came in at 52.5763 trillion won, with operating profit of 37.6103 trillion won, which - at a 72% operating margin – is an extraordinary figure for a hardware manufacturer. Nvidia CEO Jensen Huang has named SK Hynix as Nvidia's “largest memory partner”3, with a number of supply-chain analysts estimating that SK Hynix would hold roughly 60% to 70% of Vera Rubin HBM4 volume after Samsung, SK Hynix, and Micron all passed certification to supply HBM4 for the platform on June 5, 2026. Altogether, this is buttressed by the fact that SK Hynix has long been a memory supplier to Nvidia from well before the AI Hype began.

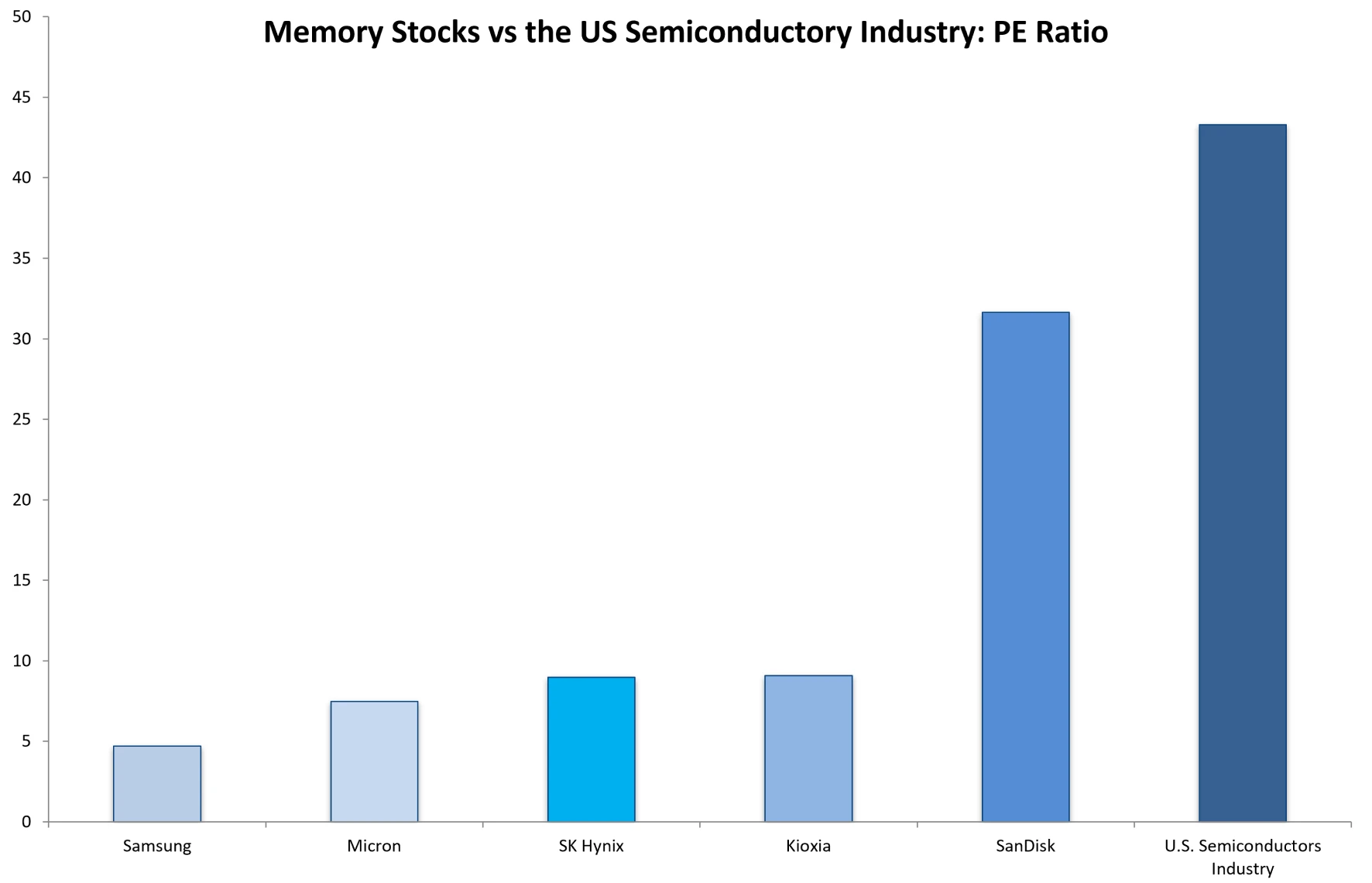

Cheapness Relative to U.S. Peers

Despite SK Hynix’s parabolic share price move in the YTD, SK Hynix's forward P/E (“Price-to-Earnings”) sits under 10x, which is well below the semiconductors industry’s media P/E even after the year's run — a gap bulls argue is unsustainable once American capital can access the stock directly.

Source: Refinitiv, S&P Global Market Intelligence, Simply Wall Street, Themes ETFs analysis. Data as of June 30, 2026

This valuation gap is, not coincidentally, the company's own stated rationale for going to Nasdaq. After filing for the ADR listing SK Hynix stated4 that the listing should help expand its investor base, and that it anticipates trading alongside rival Micron will give it the opportunity to be valued in line with U.S. peers. SK Hynix also stated that it expects to elevate its status as a global company by broadening its touchpoints in the United States, the epicenter of AI technological innovation.

At the high end, SK Hynix’s debut makes it one of the largest ADR offerings ever - surpassing Alibaba's $21.8 billion 2014 New York debut and ranking among the top five share sales in history. Proceeds are earmarked entirely for capacity: construction of the Yongin Semiconductor Cluster's Phase 1 fab, alongside the Cheongju advanced-packaging plant and EUV tool purchases.

What the ADR Listing Changes

From the bullish investor’s perspective, the ADR listing is expected to be followed by three structural changes

- A deeper investor pool can finally hold the stock directly rather than through GDRs or limited cross-border access

- Direct comparison with Micron on Nasdaq could compress the valuation discount which long-standing bulls contend is unjustified

- The capital raised materially de-risks the Yongin buildout, which is the single largest swing factor in whether SK Hynix can defend its market share against Samsung’s HBM4 catch-up attempt.

Despite a late-June selloff that wiped out roughly 174 trillion5 won of value in a single session, investors bullish on SK Hynix are positioned to argue that, despite the massive drop, HBM scarcity estimated to persist into 2027–2028 coupled with the re-rating done by the ADR listing makes the pullback more of an entry point rather than the top.

Whether this manifests or not as ADR volumes trade and stabilize is, of course, the $20+ billion question. For the bullish investor with a conviction in SK Hynix, the Leverage Shares 2x Long SK Hynix Daily ETF (ticker: SKHX) serves amplified upside by seeking daily investment results, before fees and expenses, corresponding to 200% (2x) of the daily performance of SK Hynix’s ADR.

Investors should bear in mind that the bear case for memory stocks in these times is simultaneously unprecedented and rich in history. Click here to read more.

Footnotes:

1Dear Future SK Hynix Stock Investors, Mark Your Calendars for July 10, Barchart, 27 June 2026

2South Korea’s biggest chipmaker SK Hynix plans to raise $29 billion via Nasdaq listing as soon as July 10, CNBC, 25 June 202

3Nvidia clinches deals with South Korean giants including SK Group to advance AI boom, Reuters, 8 June 2026

4Global DRAM and HBM Market Share: Quarterly, Counterpoint Research, 9 June 2026

5Samsung Electronics, SK Hynix shares tumble over 9% as chip rout spreads from Wall Street, CNBC, 1 July 2026