Article by Sandeep Rao

Why History Informs the Bear Case for SK Hynix

July 2, 2026 | Research Insights

South Korean chipmaker SK Hynix – spun off from Hyundai in 2003 and acquired by SK in 2011 – is aiming to make one of the largest ADR offerings ever on US shores after achieving triple-digit percentage gains in the year till date (YTD) in its domestic bourse. After filing for the ADR listing, the company stated1 that the listing should help expand its investor base, and that it anticipates trading alongside rival Micron will give it the opportunity to be valued in line with U.S. peers. SK Hynix also stated that it expects to elevate its status as a global company by broadening its touchpoints in the United States, the epicenter of AI technological innovation.

The objective stated bears examining as well as the intricacies of memory manufacturing that SK Hynix exclusively focuses on.

The Challenge of Investor Conviction

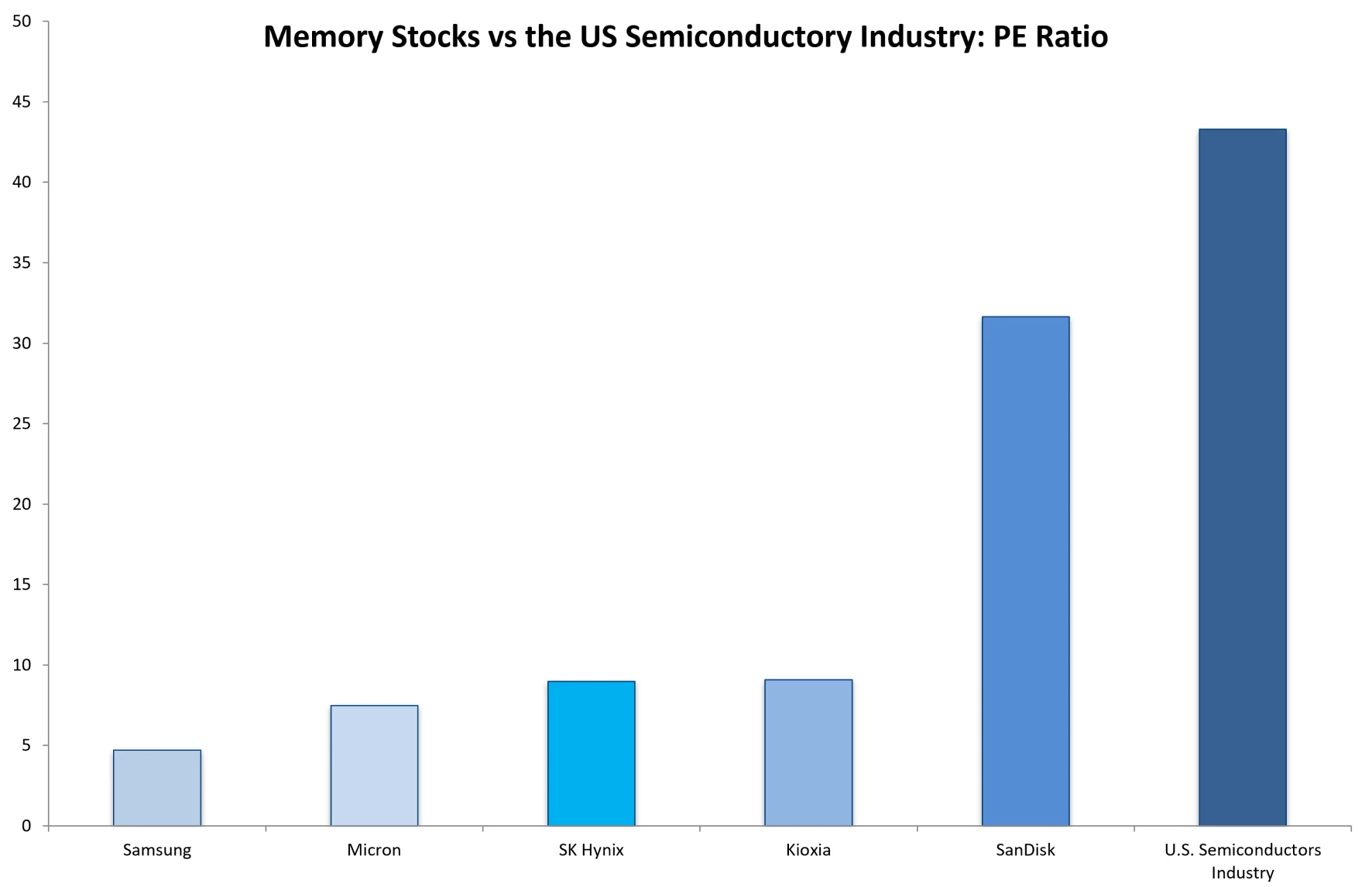

SK Hynix's forward P/E* (“Price-to-Earnings”) sits under 10x, which is well below the semiconductors industry’s media P/E even after the year's run

Source: Refinitiv, S&P Global Market Intelligence, Simply Wall Street, Themes ETFs analysis. Data as of June 30, 2026

Asian peer Kioxia’s P/E is of interest: like SK Hynix, Kioxia’s earnings witnessed massive growth – 103.6% over the past year – with analyst consensus forecasting around 41.8% annual growth in earnings going forward. Like with SK Hynix, the market has priced in growth trajectory rather than current earnings power.

Where Kioxia differs, however, is history: when a part of Toshiba, it invented NAND flash memory in 1987 and was first to mass-produce it in 1991 in collaboration with SanDisk. Kioxia’s BiCS (Bit Cost Scalable) stacking technology is proprietary, now in its 10th generation at 332 layers, with each generation incorporating Kioxia-developed innovations in cell geometry and power management.

Its most important recent architectural advance – CBA (CMOS Directly Bonded to Array) technology — was co-developed with Western Digital, which had once acquired SanDisk in 2016 only to spin it off in 2025. Kioxia runs nine fabs in Japan via a joint venture with SanDisk, with which it has decades of shared and co-developed Intellectual Property (IP). With Western Digital also stepping up to the plate in the datacenter business in recent times, Kioxia is now effectively part of a complex triumvirate that effectively pools resources and apportions profits in a pattern established over decades.

The P/E differential between SanDisk and Kioxia – and, for that matter, SK Hynix – lies in its customer engagement. After it was spun off, SanDisk ended Q3 FY2026 with three signed “New Business Model” agreements and signed two additional ones in Q4 mostly comprising of long-term supply contracts with hyperscalers and enterprise customers that lock in volume at negotiated pricing, reducing the commodity-cycle exposure that typically compresses memory multiples.

Kioxia operates long-term agreements (LTAs) for volume supply with larger customers with quarterly price negotiations. Thus, it retains upside in a rising price environment but carries full downside exposure when prices fall. While this is a strength in the current supercycle, it’s a liability in a downturn. Like most memory manufacturers, Kioxia confirmed2 right at the start of the year that supply for 2026 and is employing something of a “gentleman’s agreement”: rather than adopting a “first-come, first-served” or “everything to the highest bidder” approach, it remains committed to existing contracts. In the short term, Kioxia is arguably leaving money on the table relative to what a pure spot-pricing strategy would yield. However, in the long term it builds the kind of sticky customer relationships that can survive downturns.

Meanwhile, SK Hynix pursues both SanDisk-styled contracts known as “Advance Volume Agreements” as well as 3-5-year LTAs like Kioxia. It also secured what is arguably an industry-first along with Micron: hundreds of millions of dollars in prepayments for HBM allocation through the end of the decade. SK Hynix also secured exclusive supply qualification3 for Microsoft’s in-house Maia 200 AI chip.

While it is true that the US equity universe tends to be magnify these sorts of developments more so than Asian markets generally do, an unmissable empirical observation needs to be made – which particularly resonates across Asia: the memory industry has been one of the most historically violent cyclical sectors in semiconductors.

30 Years of Implosions

Since the nineties, there have been four distinct major crashes – each with its own trigger, and a near-consistent pattern.

In the mid-1990s, the DRAM (“Direct Random Access Memory”) market in the had 20+ players across the world. After roughly 50 fab construction plans were announced during 1995–1996 alone, DRAM prices peaked and crashed from pure overcapacity. Stock prices of memory companies fell 60–80% from peak to trough, and the resulting shock contributed to the Asian Financial Crisis that pushed South Korea into a deep recession.

In South Korea, LG Semicon and Hyundai Electronics were forcibly merged by the government due to significant losses to eventually become Hynix. In Japan, NEC and Hitachi’s DRAM operations were combined to form Elpida. In the US, Micron acquired Texas Instruments’ memory business. In Europe, Siemens spun off Infineon (IFX), which itself later spawned Qimonda — which went bankrupt in 2009.

In the 2001 dot-com collapse, several of the smaller Taiwanese and German players never fully recovered as per-megabit pricing fell well below production costs due to oversupply. Hynix in fact fell into such distress that it planned to sell itself to Micron Technology, but the deal fell through

The sharp appreciation of the Japanese yen after the 2008 financial crisis delivered a definitive blow to Japan’s memory industry: Elpida filed for bankruptcy – the largest in Japanese manufacturing history at the time - and was acquired by Micron. Qimonda filed for insolvency in January 2009.

By 2020, only a handful of memory names remained worldwide who – again – ramped up production on the back of strong demand from 2019 through the COVID years. New fabs typically cost around $15–20 billion and take 2–3 years to build. Once built, the economics favour running it at maximum utilisation due to enormous fixed costs. Thus, manufacturers must keep producing into a falling price environment long after it becomes rational to stop. In 2022-2023, demand collapsed and manufacturers once again sold chips below cost. Samsung posted a 69% fall in profits in Q4 2022, Micron saw an 88% revenue decline and a net loss of $195 million in its first fiscal quarter of 2023, and SK Hynix posted a full-year 2023 net margin of approximately negative 28%.

Is This Time Any Different?

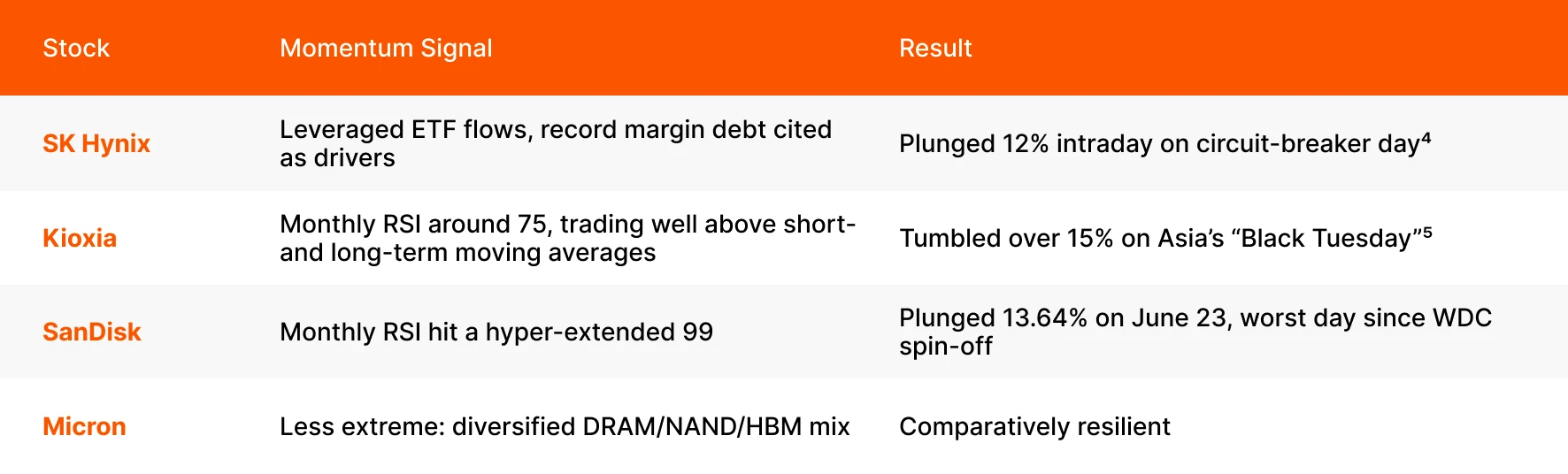

Among all memory stocks, Micron is arguably the only one that is generally considered relatively resilient:

Source: Themes ETFs analysis, as of June 25, 2026

The irony is that both Samsung and Micron have diversified revenue segments – and are thus potentially discounted for not being “all in” on AI.

The current cycle seems to be signalling investors that “this time is different” while every previous cycle produced the same result — with fewer companies left standing at the end. While the AI-driven demand is real to the point that practically every chipmaker has sacrificed ordinary customers in favour of the enterprise, this structurally unprecedented demand only holds as long as AI capex keeps growing. The moment a hyperscaler decides to pause or defer a data centre build, those advance volume agreements become renegotiation conversations, not ironclad obligations, and the prepayments already made don’t cover the cost of idle memory fabs running below capacity. That's the tail risk the contract structure can't fully insure against.

There are signs that this has already begun with OpenAI pulling back4 its IPO date while contending that the government needs5 to hold a stake in AI companies, and opposition to datacenters6 becoming strong enough to become political positions of consequence to elections in the U.S. – where the vast majority of datacenter projects are.

While it is possible that SK Hynix’s ambition to attract higher price ratios will come true, the question that will remain is how long. The answer, going by recent events, might very well be “not long”. What follows afterwards might already be writ large in recent history.

Footnotes:

1South Korea’s biggest chipmaker SK Hynix plans to raise $29 billion via Nasdaq listing as soon as July 10”, CNBC, 25 June 2026

2Memory manufacturer Kioxia reveals its entire NAND flash production volume for 2026 is already 'sold out'”, PC Gamer, 21 January 2026

3Microsoft Deploys Maia 200 AI Chip with SK Hynix HBM3E”, The Chosun Daily, 9 April 2026

4Leveraged Product Investors Suffer 25% Losses on SK Hynix, Samsung Plunge”, The Chosum Daily, 24 June 2026

5Why is Kioxia stock surging today?”, Investing.com, 24 June 2026

6OpenAI Leans Toward Waiting Until Next Year for I.P.O.”, New York Times, 25 June 2026

7OpenAI proposes handing Trump administration 5% stake”, Financial Times, 2 July 2026

8Data center opponents have blocked or delayed projects worth nearly $130 billion in 2026, study finds”, NBC News, 12 June 2026

*P/E denotes how much the market is willing to pay today for a stock per dollar of its earnings and is calculated by dividing the current share price by the Earnings Per Share (EPS).