The SpaceX IPO on June 12 was both historic and successful. Not only was it the largest IPO in history, but it saw high demand from investors, with the stock climbing upon its arrival on the Nasdaq.

Yet while the IPO was a success, not everyone is bullish on SpaceX stock. Here’s a look at the bear case for the space powerhouse.

SpaceX’s A Valuation Defying Gravity

There is no doubt that SpaceX is an impressive business. This is a company that has a near monopoly on the commercial rocket launch front, more than 10,0001 Starlink broadband and mobile satellites in operation, and a fast-growing AI business that has deals with the likes of Anthropic and Google. It also has a CEO with an incredible track record when it comes to scaling up technology businesses. There really is nothing else like it in the public markets.

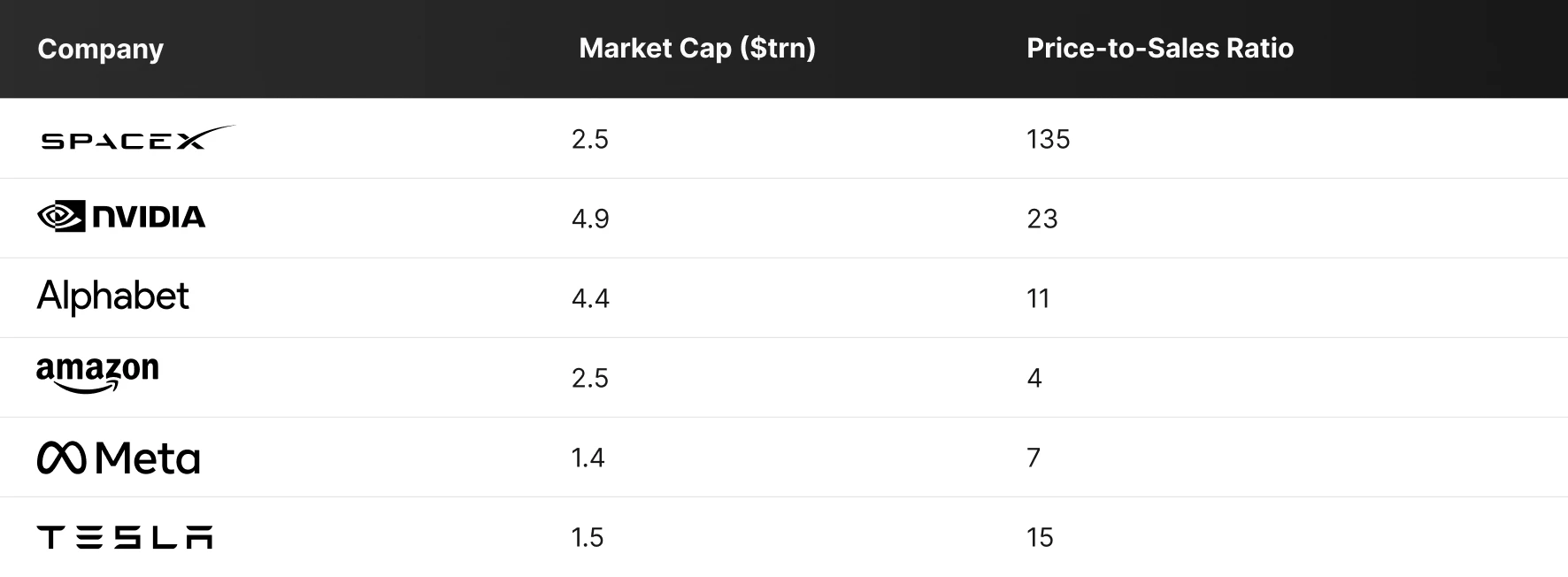

However, with this unprecedented positioning comes an equally unprecedented premium. And this is where the bears have an issue. With the company valued at around $2.5 trillion2 today, it is priced for absolute perfection. Given that revenue in 2025 was just $18.7 billion1, it is trading on a trailing price-to-sales ratio of over 130 and that kind of multiple could be hard to sustain.

Source: LSEG, as of June 17, 2026

It’s worth noting that several research firms have stated that they see the company as overvalued at current levels. One such firm is Morningstar, which believes that SpaceX is worth around $780 billion3 today (approx. $63 per share). It assigns a value of around $610 billion to the core space and connectivity businesses and then $170 billion to the AI business (a probability-weighted average of three wide-ranging AI scenarios). In its research note, it says that SpaceX faces substantial risks in relation to strategic execution, technological evolution, market dynamics, regulations, and the AI buildout.

Another firm that is bearish on SpaceX at current levels is CFRA4. It has a $115 price target and a Sell rating on the stock at present. Its analyst, Keith Snyder, says he can only match SpaceX’s current $2 trillion+ market cap by factoring in “almost comical growth for AI”. His view is that the AI total addressable market (TAM) figure quoted in the IPO prospectus ($26.5 trillion) is “wildly optimistic”.

Now, stocks can trade at high valuations for a long time. However, it’s worth pointing out that there are a few events on the horizon that could lead to a valuation reset here including:

Q2 earnings: If Starlink growth rates are disappointing and/or costs are well above estimates, investors may become less bullish on the stock.

Lock up expiration: Shortly after the first earnings report, pre-IPO investors will be free to sell a huge block of shares (7%5 of their holdings), which could put pressure on the stock.

The Anthropic and OpenAI IPOs: Investors may sell SpaceX stock to invest in these IPOs.

Free Cash Flow is Negative

Looking beyond the sky-high valuation, another component to the bear case is the company’s capital intensity and free cash flow profile.

Today, SpaceX is investing aggressively across rocket development, launch infrastructure, Starlink satellites, AI data centers, and compute clusters. As a result, it’s burning cash like there’s no tomorrow.

In 2025, for example, free cash flow was negative $13.8 billion1. Meanwhile, in Q1 of 2026, free cash flow was negative $9.1 billion1.

This means that there’s a chance that SpaceX may need to rely on external capital (e.g. debt financing or an equity raise) in the future. This could impact sentiment towards the stock at some stage – in the public markets institutional investors value operational stability.

There Are Many Operational Risks

There are also many operational risks that threaten to derail the bull case. In its research note, CFRA expresses concern4 that SpaceX’s long-term strategy remains heavily dependent on Starship – the company’s next-generation, fully reusable super heavy-lift launch system (which is still moving from development toward commercial operations). This is expected to lower launch costs and be a key enabler of Starlink satellite expansion, orbital AI compute, and lunar infrastructure. But there are no guarantees that development of this rocket will go as planned. If it faces delays or technical setbacks, it could impact nearly every major growth initiative and lead to stock price weakness.

Another risk is in relation to AI growth. A core pillar of the SpaceX bull case is massive cloud-compute hosting deals. However, while the company has done major deals with Google (it’s paying SpaceX $9206 million per month from October 2026 through mid-2029 to access roughly 110,000 Nvidia GPUs) and Anthropic (this is estimated at $1.25 billion per month7) recently, there are no guarantees that these types of deals will continue. If AI deals were to dry up as compute bottlenecks ease, the company’s premium valuation could face a reality check.

SpaceX is Dependent on Elon Musk

Of course, there is also an extremely high level of “key man” risk with this stock (this is the systemic threat an organization faces if it is overly dependent on a single individual for its operational, financial, and strategic survival). In SpaceX's IPO prospectus1, it explicitly states that Elon Musk's leadership, vision, and expertise are critical to the development of its technologies and the execution of its business strategy. It also says that it does not carry any "key-person life insurance" on Musk and that if he were to step away from the business, it would significantly disrupt strategic execution. Note that if he did step away from SpaceX, it’s highly likely that investor enthusiasm would dissipate.

One other issue that the bears point to is Musk’s capacity. Given its $2 trillion+ public valuation, SpaceX needs a 100% focused, institutional CEO. The problem is, Musk is currently balancing an unprecedented list of massive, high-stakes responsibilities. Not only is he running Tesla (which is trying to bring humanoid robots to mass production) but he is also managing The Boring Company and overseeing Neuralink meaning that he is likely to face distractions that direct his attention away from SpaceX.

Competition is Heating Up

Finally, bears point to the fact that competition in the space industry is heating up. Amazon, for example, has recently launched a space service known as Amazon Leo. It already has 2008 satellites in operation and it is winning customers in the satellite broadband space (it has said that it has “meaningful” revenue commitments8 from the likes of Delta Airlines, NASA, and Vodafone). Note that Amazon just announced9 the acquisition of satellite operator Globalstar. This acquisition will enable Amazon Leo to add direct-to-device (D2D) services to its Low Earth Orbit satellite network. In addition to the agreement with Globalstar, Amazon and Apple signed an agreement to provide satellite connectivity for current and future iPhone and Apple Watch features.

Another company that could present some competition to SpaceX in the future is Rocket Lab. It is having success on the launch front, having completed around 90 launches10 with its Electron rocket, which was developed to address the shortage of dedicated, frequent, and affordable launch opportunities for small satellites. So, while SpaceX is dominating the space industry today, its near monopoly is far from permanent. In the years ahead, nimbler rivals and deep-pocketed tech giants are likely to chip away at its market share.

The Bear Case Bottom Line

In summary, much of the bear case is tied to the high valuation and the fact that SpaceX is priced for absolute perfection. This is a generational business, however, at a market cap of around $2.5 trillion, the valuation looks stretched.

While the historic June 12 IPO showed that investor interest in the company is sky-high, the public markets are notoriously unforgiving. With the stock currently trading at over 130 times sales, there is zero room for error.

Footnotes:

1SEC.gov, Space Exploration Technologies Corp., as of May 20, 2026

2Google Finance, as of June 18, 2026

3Morning Star, SpaceX: What Investors Need to Know About Its Enormous Upcoming IPO, as of June 5, 2026

4Investing.com, CFRA initiates SpaceX stock rating at sell on execution concerns, as of June 12, 2026

5Yahoo Finance, SpaceX Lockup Period: What You Need to Know About Potential Sales by Longtime Shareholders, as of June 11, 2026

6CNBC, Google to pay SpaceX $920 million a month for compute capacity at xAI data centers, as of June 5, 2026

7Reuters, Anthropic nears first quarterly profit, agrees to pay SpaceX $1.25 billion monthly for computing power, as of May 21, 2026

8Amazon News, Shareholder Letters 2025, as of April 9, 2026

9Amazon News, Amazon to acquire Globalstar and expand Amazon Leo satellite network, as of April 14, 2026

10RocketLaunch.org, Electron Vehicle Overview, as of June 20, 2026